Here is how the typical price strategy meeting goes:

“Ok, this is what I've determine based on the numbers:

Raw Materials Cost is X

Labor + Manufacturing Cost is Y,

and since we want to a 30% margin,

the price for our product will be Y.

Boom! Done!

Price is set. Let’s grab lunch” Cue handshakes and ego strokes.

Sound familiar? Unfortunately, I’m sure it does.

Now you might be asking yourself, why is this bad? Isn’t this the rational, mathematic way to determine price?

The problem with this method is that you are focussing on yourself and on internal and current industry factors. You are letting those things drive the decision-making process. You are allowing your product and your customers to be victims of these factors.

What if you did the opposite?

What if you flipped this strategy on its head?

Instead of letting your costs and margins drive the price, let the market determine what the strategic price should be for your product and work backwards from there.

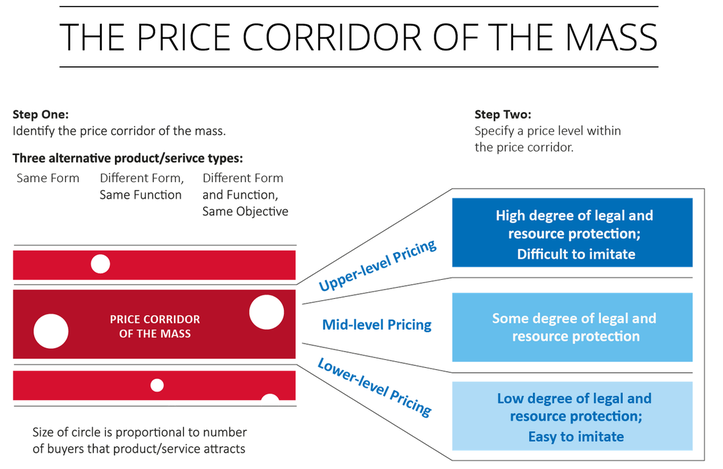

Look at the current market of your industry. What are people willing to pay for your product? Are there certain price tiers within your market, i.e. high-end, mid-range, and bargain level?

Based on this information, you can determine where in this price range you want your product to fall: upper, mid, or low.

According to the Price Corridor method developed by W. Chan Kim and Renee Mauborgne, the level of legal protection and resources at your disposal should tell you how to choose your price level.

Now that you’ve arrived at your strategic price, you can work backwards.

Take this new price and factor in your desired profit margin.

Based on this, you will know your target cost to produce a unit (including Cost of Goods Sold, Marketing, Advertising, transportation, etc).

Now the question is, can you produce a unit at this target cost? If yes, then you’re golden.

If not, you have a few options:

1) See if you can streamline your production process

Example: Henry Ford and the assembly line.

2) Look for cost innovations that will lower costs and increase value*

Example: Using a different material that is better quality and lower cost

3) Investigate possible partnerships that again, will lower costs and increase value*

Example: Outsourcing a part of your process to a company that specializes in that particular area, such as transportation or customer service.

*Notice that it says lower costs AND add value. You do not want to cheapen your product by seeking inferior alternatives just to save money. Either the product is viable at the strategic price or not. No shortcuts.

These methods are key to hitting the target cost of the product.

As with most things in life, you need to begin with the end in mind, putting other people first. In this case, you need to begin the product development cycle knowing what price you want to charge in the marketplace. This price should not be based on costs or profit margins but on what the market will accept and embrace.

Cost should be dependent on price, not the other way around.

This article is based on the work of W. Chan Kim and Renee Mauborgne from their groundbreaking Blue Ocean Strategy

“Ok, this is what I've determine based on the numbers:

Raw Materials Cost is X

Labor + Manufacturing Cost is Y,

and since we want to a 30% margin,

the price for our product will be Y.

Boom! Done!

Price is set. Let’s grab lunch” Cue handshakes and ego strokes.

Sound familiar? Unfortunately, I’m sure it does.

Now you might be asking yourself, why is this bad? Isn’t this the rational, mathematic way to determine price?

The problem with this method is that you are focussing on yourself and on internal and current industry factors. You are letting those things drive the decision-making process. You are allowing your product and your customers to be victims of these factors.

What if you did the opposite?

What if you flipped this strategy on its head?

Instead of letting your costs and margins drive the price, let the market determine what the strategic price should be for your product and work backwards from there.

Look at the current market of your industry. What are people willing to pay for your product? Are there certain price tiers within your market, i.e. high-end, mid-range, and bargain level?

Based on this information, you can determine where in this price range you want your product to fall: upper, mid, or low.

According to the Price Corridor method developed by W. Chan Kim and Renee Mauborgne, the level of legal protection and resources at your disposal should tell you how to choose your price level.

Now that you’ve arrived at your strategic price, you can work backwards.

Take this new price and factor in your desired profit margin.

Based on this, you will know your target cost to produce a unit (including Cost of Goods Sold, Marketing, Advertising, transportation, etc).

Now the question is, can you produce a unit at this target cost? If yes, then you’re golden.

If not, you have a few options:

1) See if you can streamline your production process

Example: Henry Ford and the assembly line.

2) Look for cost innovations that will lower costs and increase value*

Example: Using a different material that is better quality and lower cost

3) Investigate possible partnerships that again, will lower costs and increase value*

Example: Outsourcing a part of your process to a company that specializes in that particular area, such as transportation or customer service.

*Notice that it says lower costs AND add value. You do not want to cheapen your product by seeking inferior alternatives just to save money. Either the product is viable at the strategic price or not. No shortcuts.

These methods are key to hitting the target cost of the product.

As with most things in life, you need to begin with the end in mind, putting other people first. In this case, you need to begin the product development cycle knowing what price you want to charge in the marketplace. This price should not be based on costs or profit margins but on what the market will accept and embrace.

Cost should be dependent on price, not the other way around.

This article is based on the work of W. Chan Kim and Renee Mauborgne from their groundbreaking Blue Ocean Strategy